50/30/20 Budget Examples: Real Sample Budgets for Every Salary

See exactly how the 50/30/20 rule works with real dollar breakdowns for singles, couples, and families at different income levels.

From experience

In my own budgeting practice, I spent months failing because I was calculating my 50% needs based on my $75,000 gross salary instead of my actual $4,800 monthly take-home pay. Once I switched to budgeting based only on the cash that actually hit my bank account, the numbers finally balanced and I stopped overdrawing my checking account every single month.

The Simple Secret to Making the 50/30/20 Rule Work for You

Most financial advice tells you what to do, but it rarely shows you how it looks in the real world. If you are tired of staring at spreadsheets and wondering if you are spending too much on rent or not enough on your future, you are in the right place. The 50/30/20 rule is a powerful tool because it provides a clear budget breakdown without requiring you to track every single cent like a hawk. However, to truly master your money, you need to see how this fits into The Complete Budgeting System Guide: How to Take Control of Your Money. Once you understand the framework, the examples below will give you the visual proof you need to start today.

In practice, the biggest hurdle isn't the math-it is knowing which number to start with. Most people look at their salary and think that is their budget. But your household income is not what you actually get to spend. You have to look at your after-tax dollars, also known as your net income or take-home pay. This article will walk you through real-world 50 30 20 budget examples that account for taxes, health insurance, and different life stages. For a deep dive into the specific mechanics of this method, you can also check out The 50/30/20 Budget Rule: A Simple System for Every Paycheck before we jump into the numbers.

Why This System Works (When Others Fail)

The 50/30/20 rule works because it prioritizes balance. It splits your take-home pay into three buckets: 50% for Needs, 30% for Wants, and 20% for Savings and Debt Repayment. Unlike restrictive diets for your wallet, this method allows for a life you actually enjoy. What most guides miss is that these percentages are targets, not rigid laws. If your rent is high, you might need to adjust. If you are aggressive about debt, you might flip the script. The goal is to create a sustainable budget breakdown that prevents burnout while ensuring you aren't broke when you retire.

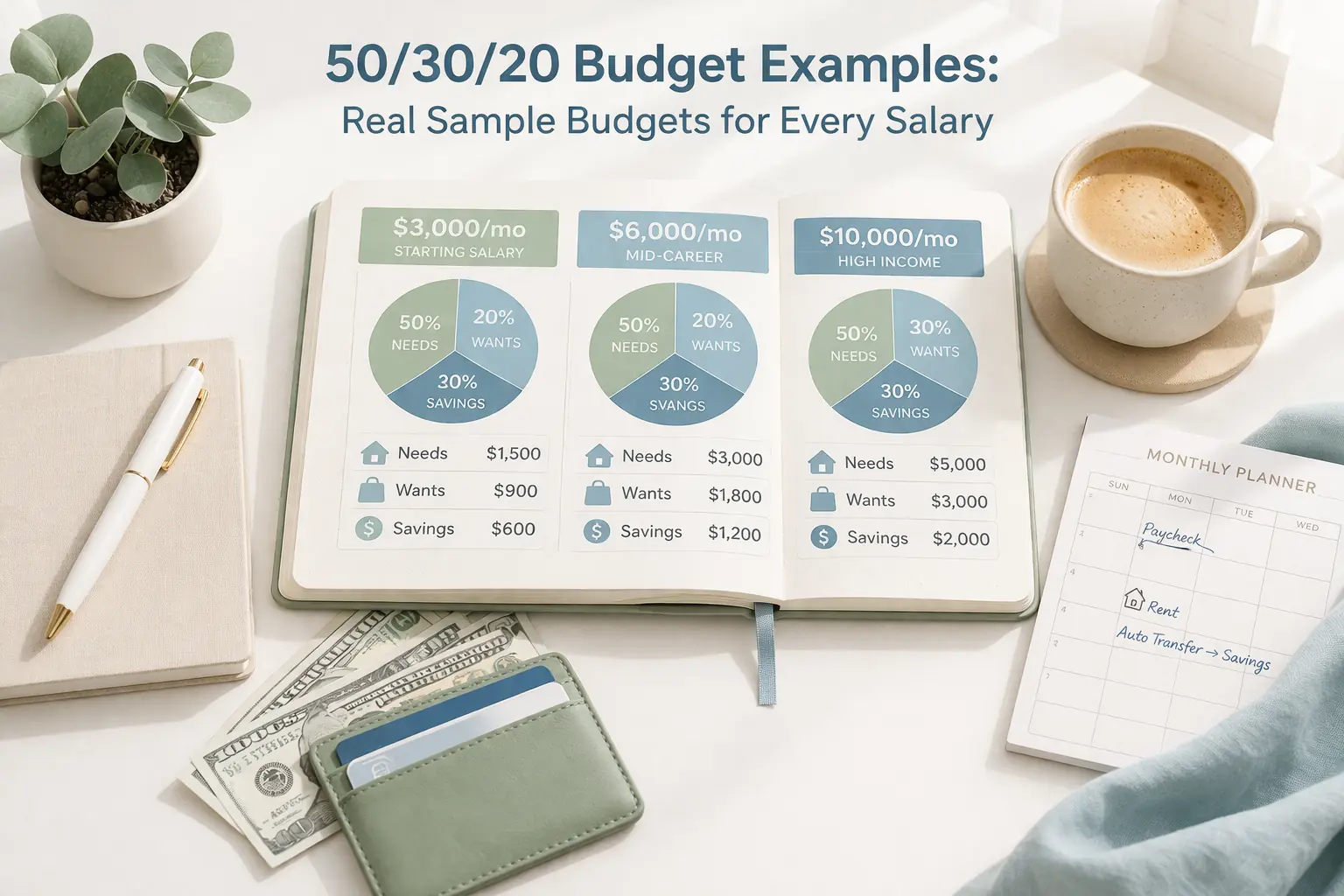

The 'Gross vs. Net' Calculator: Finding Your Starting Number

Before you can apply a percentage, you need to know your true net income. Your gross salary is the big number on your offer letter, but your after-tax dollars are what actually hit your bank account. This table helps you estimate your monthly take-home pay so you can start your 50/30/20 calculation accurately. Note: These are estimates based on average U.S. tax rates and common deductions like 401k or health insurance.

| Annual Gross Salary | Estimated Monthly Gross | Estimated Monthly Take-Home (Net) | 50% Needs Limit | 30% Wants Limit | 20% Savings/Debt |

|---|---|---|---|---|---|

| $45,000 | $3,750 | $3,000 | $1,500 | $900 | $600 |

| $65,000 | $5,416 | $4,200 | $2,100 | $1,260 | $840 |

| $85,000 | $7,083 | $5,500 | $2,750 | $1,650 | $1,100 |

| $120,000 | $10,000 | $7,800 | $3,900 | $2,340 | $1,560 |

To find your exact number, look at your most recent pay stub. Take the final amount that was deposited into your bank and multiply it by how many times you get paid per month. That is your net income. If you want to make sure you are categorizing everything correctly, refer to our Budget Categories List: Every Category You Need in Your Monthly Budget.

Real Life Example 1: The Single Professional (Net Income: $3,500)

In this scenario, we look at a single person living in a mid-sized city. Their primary focus is managing high rent while trying to build an emergency fund. Their household income is just their own salary, meaning they have full control but also full responsibility for every bill.

- Needs (50% - $1,750): Rent ($1,100), Utilities ($150), Groceries ($300), Car Insurance and Gas ($200).

- Wants (30% - $1,050): Dining out ($300), Subscriptions ($50), Hobby/Gym ($100), Shopping/Travel ($600).

- Savings/Debt (20% - $700): Student loan payment ($400), High-yield savings ($300).

The Practitioner Perspective: In my experience, singles often struggle with the 'Needs' category because they don't have anyone to split the rent with. If your needs exceed 50%, don't panic. The easiest way to fix this is to 'borrow' from the Wants category until your income grows or you find a roommate. You should also look into Sinking Funds Explained: How to Budget for Irregular Expenses to handle those yearly car registrations that often blow a single person's monthly budget.

Real Life Example 2: The Established Couple (Net Income: $6,500)

When two people combine their after-tax dollars, the 50/30/20 rule often becomes easier to manage due to shared housing costs. This couple is focused on saving for a down payment on a house while enjoying a comfortable lifestyle.

- Needs (50% - $3,250): Mortgage/Rent ($2,200), Utilities ($300), Joint Groceries ($600), Internet/Phones ($150).

- Wants (30% - $1,950): Weekend trips ($600), Date nights ($400), New furniture ($400), Streaming and Gadgets ($550).

- Savings/Debt (20% - $1,300): Retirement accounts ($800), House down payment fund ($500).

The beauty of the 50/30/20 rule for couples is the 'Wants' bucket. It allows for guilt-free spending on shared experiences without compromising the mortgage payment. To keep this on track, it is vital to Track Your Spending as a team so one person's coffee habit doesn't eat into the other's travel fund.

Real Life Example 3: The Family of Four (Net Income: $8,500)

Families face unique challenges, specifically in the 'Needs' category. Childcare, life insurance, and larger grocery bills can push the 50% limit to its breaking point. In this budget breakdown, we see how a family balances these costs.

- Needs (50% - $4,250): Mortgage ($2,500), Daycare ($1,000), Health Insurance premiums ($250), Family Groceries ($500).

- Wants (30% - $2,550): Kids' activities/sports ($500), Family vacations ($800), Dining out ($400), Entertainment/Clothes ($850).

- Savings/Debt (20% - $1,700): College savings ($500), Emergency fund ($700), Credit card debt repayment ($500).

What most guides miss: For families, the 'Needs' category often feels like it should be 60% or 70%. If you live in a high-cost area, this is normal. According to data from the Bureau of Labor Statistics, housing and transportation are the largest expenses for American households. If your needs are at 60%, simply aim for 20% wants and 20% savings. The system is a compass, not a cage.

The 'High-Cost Area' Pivot: When 50/30/20 Isn't Realistic

If you live in New York, San Francisco, or London, a 50% needs limit might seem like a joke. When rent takes up 40% of your net income by itself, you have to pivot. In these cases, we recommend the 70/20/10 shift or the 'Safety First' model.

In the Safety First model, you ensure your 20% savings/debt is met first. Whatever is left is then split between needs and wants. If your needs are 65%, your wants must drop to 15%. This protects your future self while acknowledging the reality of expensive city living. It is a practical way to use 50 30 20 budget examples as a baseline while staying flexible.

The 'Variable Income' Strategy for Freelancers

What if your after-tax dollars change every month? Most people think the 50/30/20 rule is only for salaried employees, but it is actually the best system for freelancers. The trick is to budget based on your 'lowest' expected month. Anything you earn above that 'floor' goes straight into your 20% savings bucket. This creates a buffer that protects you during slow months. By using a baseline household income figure, you prevent 'lifestyle creep' where you spend more just because you had one good month of sales.

Step-by-Step: How to Build Your Own 50/30/20 Budget

- Calculate your Monthly Net Income: Look at your bank deposits. Do not include money that goes to taxes or 401k before it hits your account.

- Set Your Three Caps: Take your total income and multiply by 0.5 (Needs), 0.3 (Wants), and 0.2 (Savings). Write these numbers down.

- Audit Your Needs: List your non-negotiable bills. If they are over your 50% cap, look for ways to trim (like switching car insurance or meal planning).

- Define Your Wants: This is everything that makes life fun but isn't required for survival. This includes Netflix, dining out, and that fancy shampoo.

- Automate Your Savings: Move your 20% to a separate account the day you get paid. This ensures you never 'accidentally' spend your future.

Common Mistakes That Break the System

The most common mistake is mislabeling 'Wants' as 'Needs.' For example, a phone plan is a need, but the latest iPhone upgrade is a want. High-speed internet might be a need for a remote worker, but the premium HBO add-on is a want. Being honest with yourself about these categories is the difference between a budget that works and one that leaves you frustrated. Another mistake is forgetting about irregular expenses. If you don't account for annual fees or holiday spending, they will feel like 'emergencies' when they are actually just poorly planned 'needs.'

Tools to Help You Succeed

You don't need fancy software to manage a 50/30/20 budget. A simple pen and paper work, but for those who want more control, consider these options:

- The Three-Account Method: Have one bank account for Needs, one for Wants, and one for Savings. When you get paid, split the money immediately. When the 'Wants' account is empty, you stop spending until next month.

- Spreadsheets: A simple Google Sheet can track your percentages automatically.

- Cash Envelopes: For the 'Wants' category specifically, using cash can help you feel the 'pinch' of spending and keep you within your 30% limit.

Conclusion: Start Where You Are

The 50/30/20 rule is about progress, not perfection. Whether you are a single person starting your career or a family managing a complex household income, seeing these 50 30 20 budget examples proves that balance is possible. Start by finding your net income, set your targets, and adjust as you go. Your future self will thank you for the discipline you show today.

Frequently Asked Questions

Is the 50/30/20 rule based on gross or net income?

The 50/30/20 rule is always calculated using your net income (take-home pay). This is the amount of money that actually hits your bank account after taxes, health insurance, and retirement contributions have been deducted.

What if my needs are more than 50% of my income?

If you live in a high-cost area or have a lower income, your needs may naturally exceed 50%. In this case, you should reduce your 'Wants' category first to cover the gap, while still trying to keep at least 10-20% for savings and debt.

Do debt payments count as needs or savings?

Minimum debt payments (like the minimum on a credit card or student loan) are considered 'Needs.' Any extra payments made to pay off the debt faster fall into the 20% 'Savings and Debt Repayment' category.

Is 401k part of the 20% savings?

Technically, yes. However, since the 50/30/20 rule is usually applied to take-home pay, most people count their 20% savings as money saved *after* their 401k is already taken out. This results in an even higher total savings rate!

How do I handle irregular bills like car registration?

You should treat these as 'Needs' but save for them monthly using sinking funds. Take the total yearly cost, divide it by 12, and include that small amount in your monthly 50% needs bucket.