The Half-Payment Method: Stop Living Paycheck to Paycheck

Learn how to split your large monthly bills into smaller, manageable bites using the half payment method to build a $1,000 buffer and end financial stress.

From experience

In practice, I spent years trapped in the "first-of-the-month" panic until I started treating my $1,400 mortgage as two $700 "micro-bills." By moving that first $700 into a dedicated bills account the moment my mid-month paycheck landed, I effectively tricked my brain into seeing a smaller balance for non-essential spending. This simple shift created a permanent $1,200 buffer in just 14 weeks, finally ending the cycle of using a credit card to cover groceries during the "lean week" before payday.

What is the Half Payment Method?

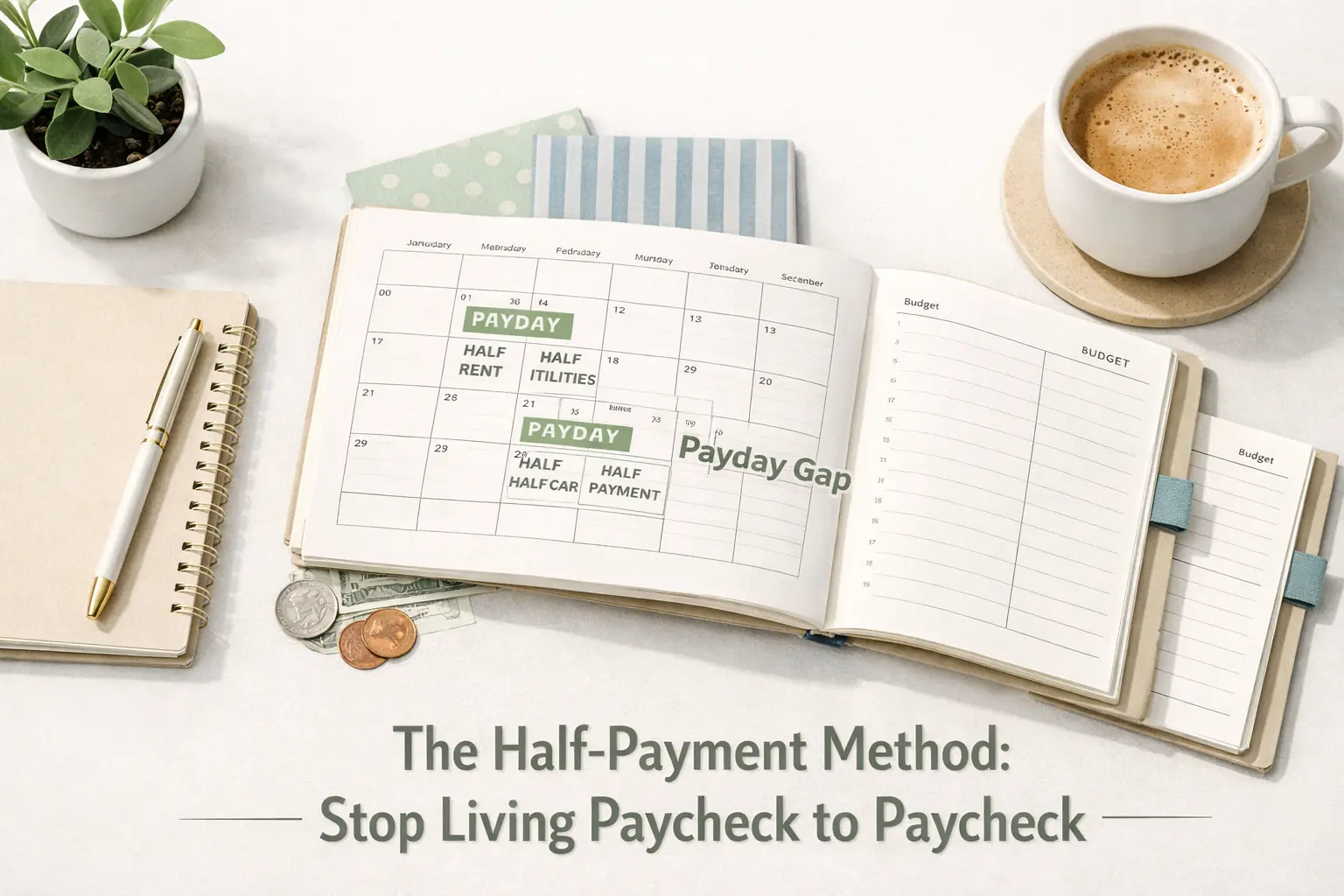

The half payment method is a simple bill management strategy designed to stop the cycle of being broke at the end of the month. Instead of waiting for a massive rent or mortgage payment to hit your bank account all at once, you divide those large monthly expenses into two smaller chunks. By setting aside half of every major bill from every paycheck, you create a consistent flow of money that prevents the stress of a empty checking account. This approach is a core part of The Complete Budgeting System Guide: How to Take Control of Your Money because it transforms how you view your cash flow from a monthly burden into a manageable biweekly routine.

For most people, the struggle is not the total amount of money they earn, but the timing of when that money leaves their hands. When you have a $1,500 rent payment due on the first of the month, but you only get paid $2,000 on the 30th, you are left with almost nothing for groceries, gas, or savings for the next two weeks. The half payment approach solves this by spreading the weight of your bills across the entire month. You are essentially paying your future self first by securing the money for your bills in smaller, bite-sized pieces.

This method is particularly effective for those who use a How to Budget Every Time You Get Paid: The Paycheck Budget System Guide because it aligns perfectly with a biweekly or weekly pay schedule. By breaking down your fixed expenses, you stop looking at your bank balance as a whole and start looking at it as a collection of earmarked funds. This simple shift in perspective is often the difference between staying in debt and finally building a savings cushion that lasts.

The Psychological Shift: Why Smaller Chunks Win

Most budgeting advice focuses on the math, but the half payment method focuses on the psychology of spending. When you see $2,000 in your checking account, your brain tells you that you are wealthy. You might be tempted to go out for a nice dinner or buy that new pair of shoes. However, if $1,500 of that money is already spoken for by rent, you aren"t actually wealthy: you are just holding someone else"s money. By splitting that $1,500 into two $750 payments, you never see that large, tempting balance in the first place.

In practice, what most guides miss is the concept of decision fatigue. When you have to decide how to spend a large sum of money once a month, you are more likely to make mistakes. When you automate a biweekly bill payment schedule, you remove the need to make those decisions. The money is moved before you even have a chance to think about spending it. This creates a psychological safety net that reduces the constant low-level anxiety associated with bill due dates.

Step-by-Step Guide to the Half Payment Method

- List All Fixed Monthly Expenses: Write down every bill that has a set due date and a set amount. This includes rent, car payments, insurance, and utilities.

- Divide Each Total by Two: If your rent is $1,200, your half payment is $600. If your car insurance is $100, your half payment is $50.

- Identify Your Pay Dates: Map out exactly when you get paid over the next three months. This helps you visualize your half payment method calendar.

- Set Up a Separate Bill Account: This is a pro tip that many beginners overlook. Open a second checking account specifically for bills. Every payday, transfer your total half-payment amount into this account and do not touch it.

- Automate the Transfers: Set your bank to automatically move the money on your payday. This ensures you never forget to set aside your portion of the bills.

By following these steps, you are effectively split bills between paychecks. This means that by the time the actual bill is due, the full amount is already sitting in your secondary account, ready to be paid. You no longer have to worry if the money will be there, because you built it up over time. This creates a natural checking account buffer that grows as you become more disciplined with the system.

The Buffer Gap Technique: A Real-World Case Study

To understand the power of this method, let"s look at Sarah, a graphic designer who was living paycheck to paycheck with $0 in her savings account. Sarah"s fixed expenses totaled $2,400 per month, and she earned $1,800 every two weeks. Before using this method, Sarah would pay all her bills out of her first paycheck of the month, leaving her with only $600 for everything else until her next payday. She often ended up using credit cards just to buy groceries.

Sarah decided to implement the half-payment strategy. In Month 1, she had to scrimp and save to set aside the first half of her rent ($600) while still paying the current month"s bills. It was a tight transition, but she managed it by cutting back on dining out for four weeks. By Month 2, she had her first $600 ready before her rent was even due. This felt like a massive win. She continued to set aside half of every bill from every paycheck.

| Month | Action Taken | Checking Buffer Balance | Financial Stress Level |

|---|---|---|---|

| Month 1 | Started splitting $1,200 rent into $600 chunks. | $0 | High | Month 2 | First full month of automation; $250 extra saved. | $250 | Medium | Month 3 | Consistent transfers; avoided a $400 car repair crisis. | $550 | Low | Month 4 | Buffer reached $1,000; bills paid 15 days early. | $1,000 | None |

By the end of Month 4, Sarah had a $1,000 buffer in her bill account. Because she was always half a month ahead on her payments, she was never caught off guard. This is the goal of the half payment method: to create a financial lead time that protects you from the unexpected. Sarah didn"t get a raise; she simply changed the timing of her bill management.

Paying Rent in Installments (Even if Your Landlord Won"t)

One of the biggest hurdles to this system is paying rent in installments. Most landlords require one lump sum on the first of the month. They don"t care about your biweekly pay schedule. However, you can still use the half payment method by acting as your own "escrow" service. You don"t actually send the money to the landlord twice a month: you send it to your own designated bill account.

For example, if your rent is $1,200, you move $600 from Paycheck A into your bill account and $600 from Paycheck B into the same account. When the first of the month rolls around, you simply pay the landlord the full $1,200 from that account. This gives you the benefit of installment payments without needing your landlord"s permission or cooperation. It turns a giant monthly hurdle into two smaller steps that are much easier to clear.

Budgeting for large monthly expenses requires this kind of foresight. If you wait until the due date to think about the money, you have already lost the battle. The half payment method forces you to think 15 to 30 days ahead at all times. This forward-thinking mindset is what eventually allows you to transition into more advanced strategies like Sinking Funds Explained: The Ultimate Method to Budget for Irregular Expenses, which handle non-monthly costs like car registrations or holiday gifts.

Mastering the Half Payment Method Calendar

The key to making this work long-term is visualization. You need to see how your paydays interact with your due dates. On a standard calendar, mark every payday with a green circle and every bill due date with a red square. You will quickly notice that some paychecks are "heavier" than others if you don"t split your bills. The half payment method levels the playing field so every payday feels exactly the same.

What most people find is that two months out of the year, they receive three paychecks instead of two if they are paid biweekly. These "magic months" are the secret weapon of the half payment method. Since your bills are already covered by the half-payments from the first two checks, that third paycheck is pure profit. You can use this windfall to jumpstart your emergency fund or pay down debt. This is a critical component of a How to Budget a Bi-Weekly Paycheck: The 2-Paycheck Calendar Method and should be planned for in advance.

Common Mistakes and How to Avoid Them

The most common mistake people make when starting the half payment method is forgetting to account for the "transition month." If you start this month and your rent is due in three days, you probably don"t have the extra cash to set aside for *next* month"s rent yet. You have to find a way to "catch up" once. This might mean using a small portion of your savings or cutting your variable spending to the bone for just one month. Once you are caught up, the system runs on autopilot.

Another mistake is keeping the bill money in your primary checking account. If you see the money, you will likely spend it. Whether it is a physical cash envelope or a digital sub-account, you must separate the bill money from your "spending" money. The government offers great resources for basic financial management at [https://www.consumer.gov](https://www.consumer.gov) which can help you understand your rights when opening new bank accounts for this purpose.

Finally, don"t forget to include your sinking funds in your half-payment math. If you know you spend $600 on Christmas every year, that is $50 a month. Split that into two $25 half-payments from every paycheck. Treating irregular expenses like fixed monthly bills is the final step in moving from a reactive budgeter to a proactive wealth builder. When you combine the half payment method with consistent tracking, you gain a level of control that most people never experience.

Conclusion: Taking the First Step

Stopping the paycheck to paycheck cycle doesn"t require a six-figure salary: it requires a system. The half payment method is the most practical way to bridge the gap between your income and your expenses. By splitting your bills, creating a dedicated account, and visualizing your calendar, you remove the drama from your finances. Start today by looking at your largest bill and committing to saving just half of it from your next paycheck. That single step is the beginning of your journey toward a $1,000 buffer and the peace of mind that comes with knowing your bills are always covered.

Frequently Asked Questions

What if I get paid weekly instead of biweekly?

You can simply adapt the method by using a quarter-payment system. Divide your monthly bills by four and set that amount aside from every weekly paycheck. The logic remains the same: smaller, more frequent contributions are easier to manage than one large payment.

Does this method work for variable bills like electricity?

Yes, but it requires a slightly different approach. Look at your highest bill from the previous year and use that as your baseline. Set aside half of that "peak" amount every paycheck. During months when the bill is lower, the extra money stays in your account as a buffer for the more expensive months.

Do I need a special bank account for the half payment method?

While not strictly required, having a separate checking account for bills is highly recommended. It creates a physical barrier between the money you need for rent and the money you use for groceries, which prevents accidental overspending.

What happens during a three-paycheck month?

In a three-paycheck month, your bills are already covered by the first two paychecks. This makes the third paycheck a "bonus" that can be used to fund your emergency savings, pay down high-interest debt, or invest for the future.

How do I handle bills that are due at the very beginning of the month?

This is the core purpose of the method. You save the first half from your last paycheck of the *previous* month and the second half from the first paycheck of the *current* month. This ensures the money is ready and waiting before the due date arrives.